2025 year in review and 2026 outlook

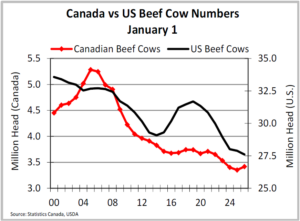

April 17, 2026Canadian cattle and beef prices are set in the much larger U.S. market. Price pressure will come when the US herd turns. US cattle and calves on January 1, 2026 were down 0.4%, with beef cows down 1%. The spotty weather and higher borrowing costs are working against the industry restocking after drought. Setting up tight supplies and strong prices for the coming year.

The Canadian cattle herd on January 1st was up 2.5% from 2025. The increase in beef cow numbers in the west (+2%) were slightly larger than in the east (+1.6%). Beef breeding heifers were also larger in the west (+4.9%) compared to the east (+3.6%), pointing to a slightly more aggressive approach by western Canadian producers as they looked to take advantage record setting prices.

Inventories of calves and yearlings were supported by record large net feeder trade. In 2025, Canada was a net feeder importer of 440,000 head, almost 145,00 head larger than 2024. This has allowed beef breeding heifer numbers to increase while at the same time providing a larger supply of calves and feeder cattle for the feedlot industry. On January 1, Canada accounted for 11% of the North American beef cow inventory.

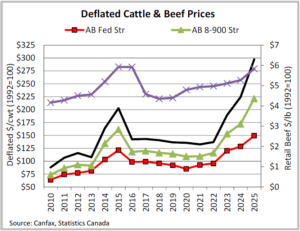

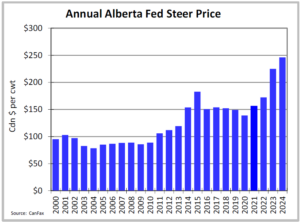

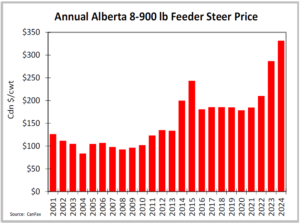

Cattle prices spiked to new record highs in 2025. Alberta fed steer prices were up 16%. Alberta 850 lb feeder steers climbed 29% in 2025 with Alberta 550 lb steer calves up 33%. Average deflated prices for Alberta fed steer, feeder steer and steer calf prices were 23%, 37%, and 47% above their previous respective highs set in 2015. Deflated cow-calf returns were also estimated to be record large in 2025, supporting expansion.

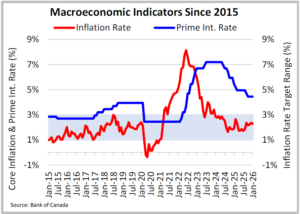

The Bank of Canada’s prime interest rate drifted lower throughout 2025. However, the annual average was still two percentage points higher than in 2015. This requires a larger proportion of revenue to support debt repayment and is expected to slow herd expansion in this cycle. A slower expansion phase will support prices for longer, as long as demand holds up.

The Canadian unemployment rate averaged 6.9% in 2025, the highest since 2016 (omitting 2020 and 2021). A December survey found that hiring managers noted a skills gap, in both hard and soft skills, as they struggled to fill positions.

Bottom line: The Canadian herd has turned and is entering the expansion phase. However, interest costs are notably higher than during the 2015 expansion phase. Weather remains the biggest unknown. Expectations are for a slower turn for the North American herd.

2025-26P BARLEY SUPPLY AND DISPOSITION

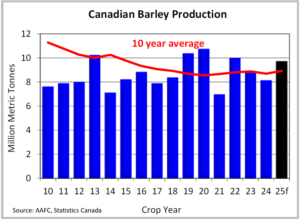

- Canadian barley production was 9.7 million metric tonnes in 2025, up 19% from 2024, and up 9% from the five-year average.

- Barley exports in 2025-26 are projected to be up 18% from 2024-25. Total domestic use in 2025-26 is projected at 6.1 million metric tonnes, up 13% from 2024-25.

- Ending stocks in 2025-26 are projected at 1.6 million metric tonnes, up 28% to be the largest since 2016. The stocks-to-use ratio is projected at 26%, also the largest since 2016. Keeping prices under pressure.

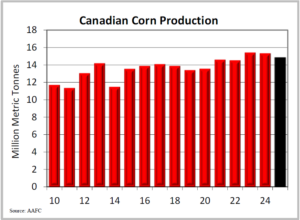

2025-26P CORN SUPPLY AND DISPOSITION

- Canadian corn production was 14.87 million metric tonnes, down 3% from 2024-25 and was the third largest on record.

- Exports in 2025-26 are projected at two million metric tonnes, down 28% from 2024-25. Total domestic use in 2025-26 is projected at 14.8 million metric tonnes, steady with 2024-25.

- Ending stocks in 2025-26 are projected at 1.6 million metric tonnes, up 1% from 2024-25. The stocks-to-use ratio is projected at 11%, compared to the five-year average of 13%.

FEED GRAIN PRICES

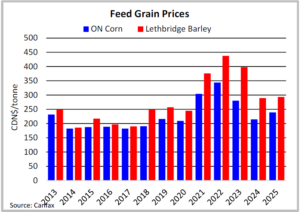

- Lethbridge barley averaged $293/tonne in 2025, up 1% from 2024, up 3% from the 10-year average, but down 16% from the five-year average. Lethbridge barley was mostly steady near $310/tonne through the first half of the year. Prices softened immediately prior to the 2025 harvest, bottoming near $257/tonne in October before rebounding higher to end the year.

- Lethbridge barley was priced competitively against Alberta oats in 2025, but not against Omaha or Ontario corn.

- Ontario corn averaged $239/tonne in 2025, up 12% from 2024, up 3% from the 10-year average but down 12% from the five-year average. Ontario corn was in a tight range of $225- 250/tonne in 2025, with a ‘V’ shape, bottoming in August.

- Omaha corn averaged C$253/tonne in 2025, up 2% from 2024, up 14% from the 10-year average, but down 15% from the five-year average.

HAY PRICES

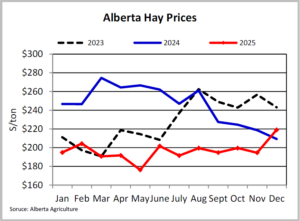

- Alberta hay prices averaged $197/ton ($217/tonne), down 20% from 2024 and 6% below the five-year average, but up 15% from the 10-year average.

- Alberta hay was largely rangebound from $180-200/ton, with little variation except in December, when prices spiked to near $220/ton.

- Montana hay prices averaged US$126/ton (C$219/tonne) in 2025, a C$20/ton discount to Alberta.

Bottom line: Record large global corn production has kept pressure in the feed grain market. Even with the increase in feed costs, cost of gain remains economical for Alberta and Ontario feedlots.

SLAUGHTER

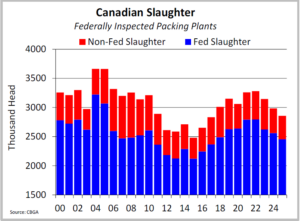

- Domestic (Federally Inspected) slaughter was 2.86 million head in 2025, down 4%, to be the smallest since 2017.

- Fed slaughter was 2.45 million head, down 4%. Non-fed slaughter was 400,100 head, down 5%.

- Cow marketings in 2025 were the smallest on record going back to 2005 as the Canadian beef cow herd moved into rebuild.

- Packer Utilization averaged 84% for the year and remain in the healthy range for this phase of the cattle cycle.

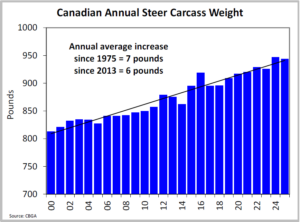

CARCASS WEIGHTS

- Despite the US continuing to see large year over year gains in carcass weights in 2025, to offset smaller numbers. Canadian steer carcass weights averaged 944 lbs in 2025, three pounds lighter than 2024. However, weights were heavier for heifers, cows, and bulls offsetting some of the reduced slaughter.

- In the West, steer weights were notably heavier during the fourth quarter. In the East, weights were steady (excluding the six weeks during the 2024 shutdown).

BEEF PRODUCTION

- Domestic beef production declined 3% in 2025. Fed production was down 4% with non-fed production down 3%.

- Live slaughter exports were down 5%.

- Total beef production (domestic, live slaughter exports and offals) was down 4% to 3.36 billion pounds.

BEEF/CATTLE EXPORTS

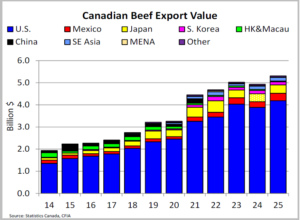

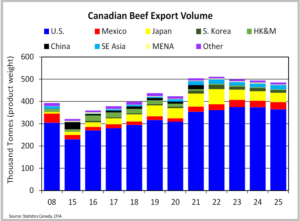

- In 2025 beef exports were down 2% at 486,100 metric tonnes; and up 8% to $5.31 billion. Export volumes declined for the third consecutive year; however, the value of those exports was the highest on record. The top five destinations by market share were the U.S. (75%), Japan (8.5%), Mexico (7%), Southeast Asia (4%), and South Korea (3%).

- Live cattle exports at 692,900 head in 2025, were down 5% from 2024. Fed exports were down 5% with non-fed exports down 12%. Feeder exports were up 5% to 108,000 head.

BEEF/CATTLE IMPORTS

- In 2025, beef imports were up 21% to 252,900 metric tonnes; and up 28% to $2.83 billion.

- Canada’s top five suppliers were the U.S. (35%), Australia (21%), New Zealand (14%), the EU and U.K. (8%), and Mexico (5%).

- In 2025, feeder imports were up 36% to 544,300 head. Leaving Canada a net feeder importer of almost 440,000 head. Larger imports have supported feedlots while allowing the beef breeding herd to increase.

Bottom line: Domestic beef production in 2026 is projected to be larger than 2025 supported by the additional feeder imports. This will support domestic packer utilization. Meanwhile, the southern Plains expect to have more plant closures, reducing feedlot leverage.

DEMAND

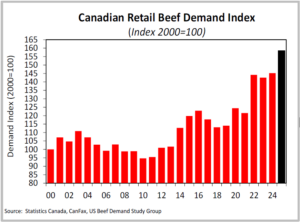

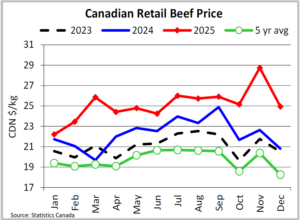

- In 2025, Canadian retail beef demand was the strongest since the mid-1980’s. Retail beef demand was supported by historically strong deflated retail beef prices, and per capita supplies. Domestic supplies have been supported by larger beef imports.

RETAIL PRICES/CONSUMPTION

- Nominal retail beef prices in 2025 were 13% higher in 2024 and 27% higher than the five-year average; deflated prices were 11% and 16% higher respectively.

- Deflated retail pork and chicken prices were both up 4% from 2024. But have been relatively stable compared to beef’s climb.

- The beef-to-pork price ratio averaged 2.46:1 in 2025, the beef-to-chicken price ratio averaged 2.54:1.

QUALITY GRADING

- Prime and AAA grading averaged 79% in 2025, providing a consistent high-quality product to the marketplace.

- The increase in the proportion of Prime and AAA graded beef has put some unconventional cuts on menus and has provided more price-friendly options at the meat counter for a wider range of consumers.

FED PRICES

- Alberta fed steers averaged $292/cwt in 2025, 19% stronger than 2024. The first quarter was marked by tariff threats, limiting any seasonal increase. Counter seasonal summer strength was driven tight supplies due to the U.S.-Mexican border closure in July and punishing tariffs on Brazilian beef in August. Ontario fed steer prices were 24% stronger.

- Feedlot margins on the cash market with no risk management in 2025 were estimated to be positive for all classes of cattle.

FEEDER PRICES

- In 2025, Alberta 550 lb steer calves averaged $578/cwt, up 35% from 2024. Ontario steer calves averaged $551/cwt, up 34%, and U.S. steer calves averaged C$551/cwt up 30%.

- In 2025, Alberta 550 lb steer calves averaged a $27/cwt premium to both Ontario and U.S. calves, encouraging imports.

- In 2025, Alberta 850 lb steers averaged $432/cwt 30% stronger than 2024 with Ontario at $440/cwt and the U.S. at C$423/cwt. Alberta 850 feeder steers averaged an $8/cwt discount to same-weight Ontario steers but an $8/cwt premium to the U.S.

Bottom line: Beef is in the middle of a significant ‘protein moment’, and this is expected to continue into 2026. The revamped USDA food guide is anticipated to support beef demand on both sides of the Canadian-U.S. border. To date, prices have been supported by strong demand. That is expected to switch in 2026 to a rationing of supplies. Feeder prices are anticipated to remain strong, with no current timeline to re-open the Mexican border. Producers should expect price volatility with announcements around the CUSMA review.